Fresh Features - Term Structure Richness

Term Structure Richness

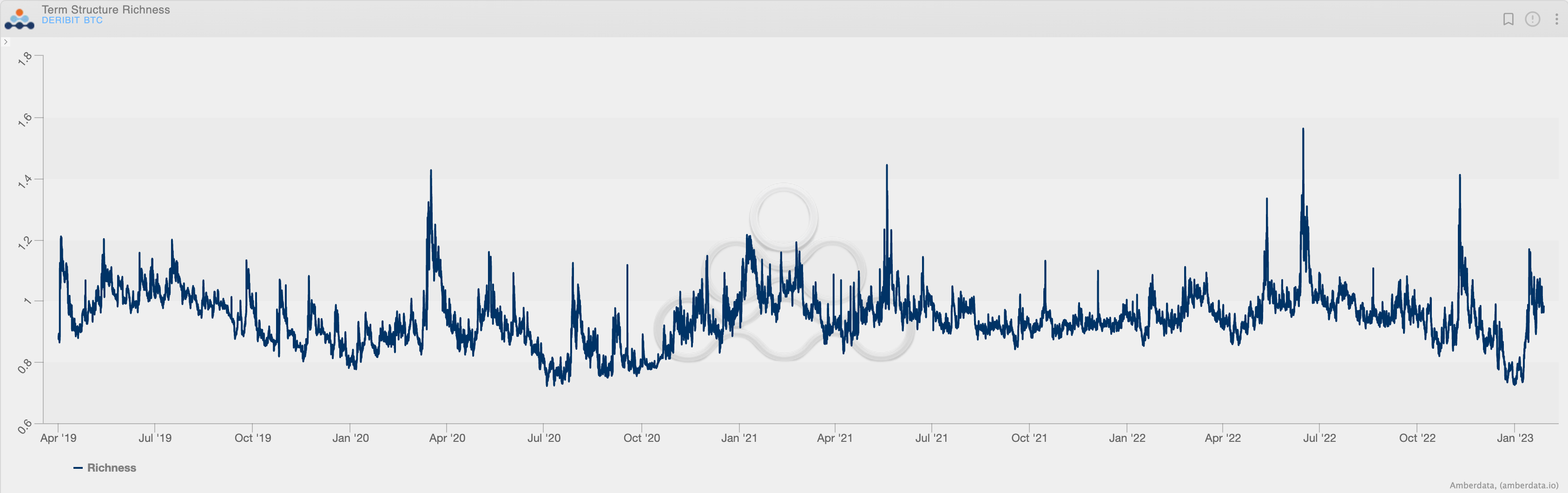

The “Term Structure Richness” is the relative “level” of the Contango or Backwardation shape. A reading of 1.00 would be a perfectly flat term structure - as measured by our method - while readings below/above represent Contango/Backwardation respectively. Using the term structure levels enables us to quantify how extended the term structure pricing currently is, at any point in time.

Straight out from our recently released report, link here, the extent of Contango/Backwardation is measured using the relative spreads of 7-day, 30-day, 60-day, 90-day, 180-day ATM volatilities.