Crypto Options Analytics, September 12th, 2021

Visit gvol.io

Disclaimer: Nothing here is trading advice or solicitation. This is for educational purposes only.

Math minded people here, pardon any typos.

| Twitter")

Feel free to contact us at https://t.me/tradeparadigm & follow us at @tradeparadigm on Twitter to access the best pricing and liquidity for large trades in crypto derivatives.

$45,907

DVOL: Deribit’s volatility index

(1 month, hourly)

SKEWS

(Sept. 12th, 2021 - Short-term and Medium-Term BTC Skews - Deribit)

Monday started the week with a sharp sell-off in spot prices. This move had been partially telegraphed by the options market prior to this week, as option skews hit par, despite rallying in spot prices.

As prices dropped this week, option skews quickly broke into negative territory, lead by short-term and medium-term options.

Long-term options also saw skews dip, but only slightly and quickly recovered.

The long-dated option skews are telegraphing sustained market demand for upside volatility, something bullish for the price trends in the larger picture.

(Sept. 12th, 2021 - Long-Dated BTC Skews - Deribit)

TERM STRUCTURE

(Sept. 12th, 2021 - BTC’s Term Structure - Deribit)

The term structure saw a lot of flattening early in the week due to the demand for short-term put protection.

As spot prices stabilized, the term structure resumed its persistently steep Contango formation.

Dec. 31st expiration continues to be relatively expensive and an enticing maturity to sell implied volatility.

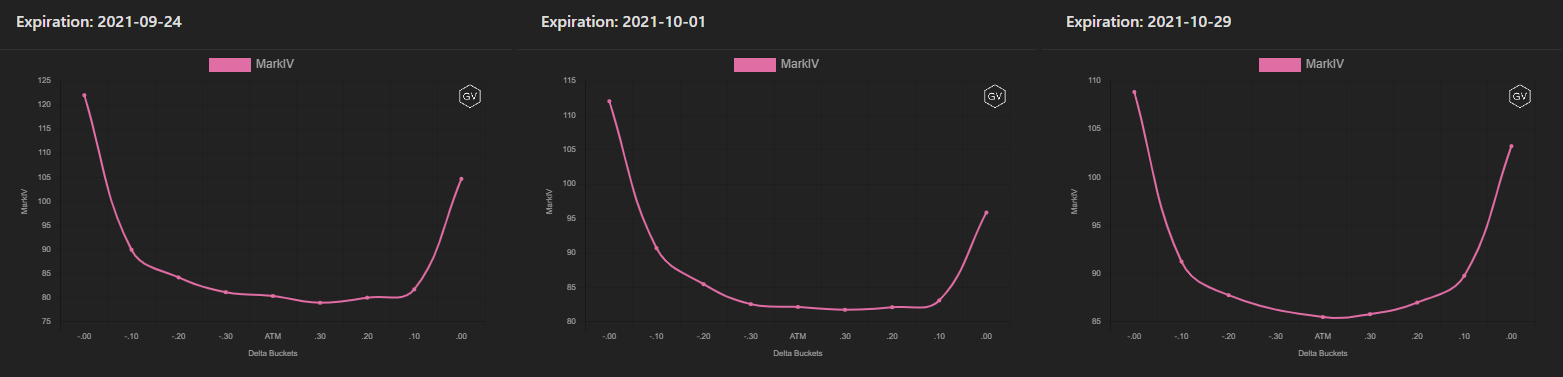

ATM/SKEW

(Sept. 12th, 2021 - BTC ATM & Skews for options 10-60 days out - Deribit)

ATM IV (left) displayed erratic behavior this week (or high vol-of-vol). The sharp rally in ATM IV isn’t surprising given the spot price action, but the quick reduction in volatility shows that option traders think the sell-off is likely done for now.

SKEW (right) has consistently dropped lower throughout the month and put IV has finally gained enough favor to send overall skew into negative territory. If this sell-off is indeed stabilizing, negative IV will likely return to par in the next week or so.

VOLUME

(Sept. 12th, 2021 - BTC Premium Traded - Deribit)

(Sept. 12th, 2021 - BTC’s Contracts Traded - Deribit)

Option volume saw a decent spike due to the drop in spot prices, but this uptick in option volumes was short lived.

Without any sustained increase in option demand, we continue to think BTC will see relatively sleepy activity compared to ETH.

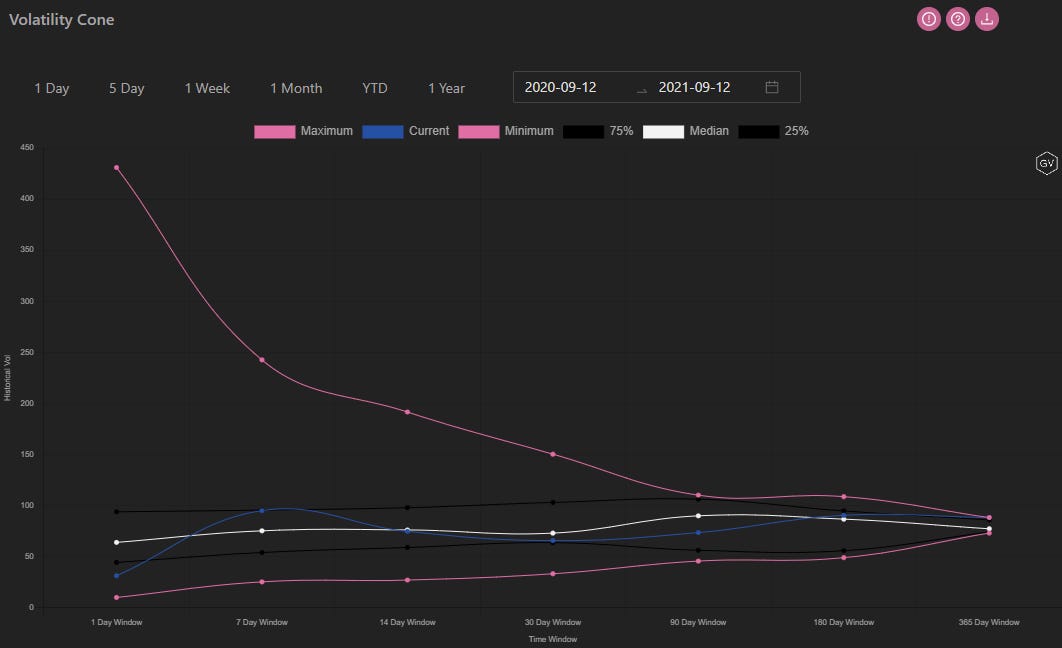

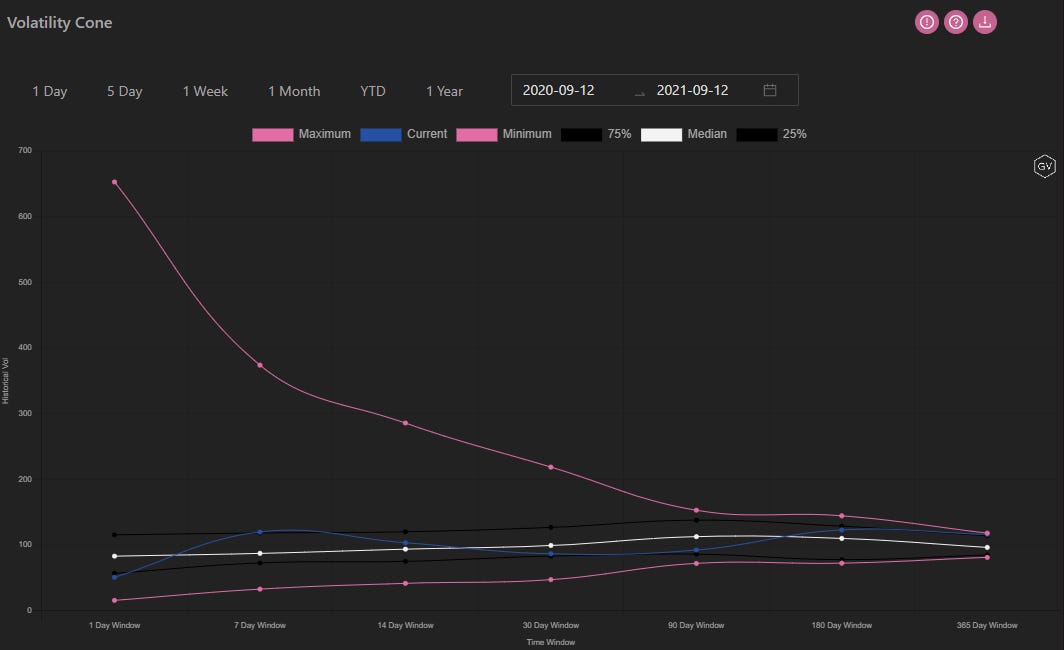

VOLATILITY CONE

(Sept. 12th, 2021 - BTC’s Volatility Cone)

To no surprise, realized volatility saw a sharp increase as spot prices quickly dropped early in the week.

With the exception of 7-day RV, which perfectly captures the mood this week, most RV measurement windows are flirting with the median.

Assuming spot prices hold above their recent lows, RV will likely return to the lower 25th percentile as BTC works the $45k-$50k price range.

REALIZED & IMPLIED

(Sept. 12th, 2021 - BTC’s 10-day Realized-, and Trade-Weighted-, Implied-Vol.-Deribit)

Long Vol. traders paid a lot of carry, through theta decay and term-structure “roll”, but were finally vindicated this past week.

The large IV/RV premium, which has persisted over the past few weeks, finally narrowed to zero as RV caught-up to IV this past week.

$3,430

DVOL: Deribit’s volatility index

(1 month, hourly)

SKEWS

(Sept. 12th, 2021 - ETH’s Skews - Deribit)

ETH option skews saw a dip lower as spot prices dropped early in the week.

Like BTC, short-term and medium-term option skews are the most negative.

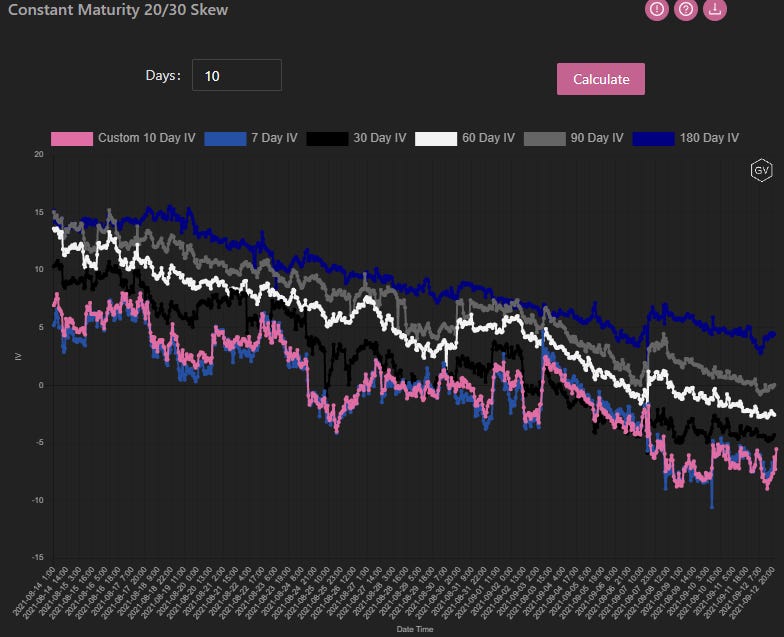

Something somewhat surprising is the “steady” drop lower in ETH skews across the board; there doesn’t seem to be a slow down either. This can be observed in the constant maturity chart below.

Hopefully, this trend can turn around.

(Sept. 12th, 2021 - ETH’s Skews - Deribit)

(Sept. 12th, 2021 - ETH’s Skew Constant Maturity Chart - Deribit)

TERM STRUCTURE

(Sept. 12th, 2021 - ETH’s Term Structure - Deribit)

The term-structure, although currently in Contango, has been able to flatten versus last week.

There is still “roll-down”, especially considering the expensive Dec. expiration, but overall the term-structure isn’t as steep as recently seen.

ATM/SKEW

(Sept. 12th, 2021 - ETH’s ATM & Skews for options 10-60 days out - Deribit)

ATM IV (left) saw a brief spike as spot prices dropped, but overall ETH IV seems to be able to hold these higher levels. Option traders are pricing in some volatility in ETH going forward.

SKEW (right) is showing a steady drop lower. The skew is now negative for these select expirations and the grind lower seems steady and persistent.

VOLUME

(Sept. 12th, 2021 - ETH’s Premium Traded - Deribit)

(Sept. 12th, 2021 - ETH’s Contracts Traded - Deribit)

ETH option volumes saw a large spike higher due to the drop in spot prices.

It’s interesting to note that very little of the volume on the spike was block-traded.

VOLATILITY CONE

(Sept. 12th, 2021 - ETH’s Volatility Cone)

Realized volatility is displaying a similar profile to BTC.

As long as ETH holds these recent lows, we’re likely to see ETH RV going back towards the lower 25th percentile as ETH works back up and through $4k.

REALIZED & IMPLIED

(Sept. 12th, 2021 - ETH’s 10-day Realized -, and Trade-Weighted-, ImpliedVol.-Deribit)

The IV / RV premium actually inverted this week.

The gap between IV/RV has been narrower for ETH than BTC in general, but option buyers did have to endure heavy decay until this week nonetheless.

IV is now pricing in lower RV in the near future.

could you tell me what it means for skew to be "negative"? i see the chart below zero, but i'm not sure what's being subtracted from what there.

amazing info as always ... thanks!