Crypto Options Analytics, Jan 23rd, 2022

Visit gvol.io

Disclaimer: Nothing here is trading advice or solicitation. This is for educational purposes only.

Math minded people here, pardon any typos.

| Twitter")

Feel free to contact us at https://t.me/tradeparadigm & follow us at @tradeparadigm on Twitter to access the best pricing and liquidity for large trades in crypto derivatives.

DeFi Options

DOVs

One of the recent themes in the crypto options market is structural short volatility flow via “DOVs” (DeFi Option Vaults).

Protocols such as Ribbon, Friktion, Atomic.finance and Thetanuts allow crypto holders to allocate holdings to structured products that perpetually use the capital to sell covered calls and cash secured puts on Solana, Bitcoin and EVM chains respectively.

Top Trades this week include:

RBN - AVAX 1/28 95 C = ~ $17m (Notional)

RBN - ETH 1/28 2500 P = ~ $67m (Notional)

RBN - ETH 1/28 3200 & 3300 C = ~ $82m (Notional)

RBN - BTC 1/28 44k C = ~ $1.7m (Notional)

RBN - AAVE 1/28 44k C = ~ $28m (Notional)

Frik - SOL $160 1/28 C = ~ $22m (Notional)

Frik - BTC $45k 1/28 C = ~ $16.2m (Notional)

Frik - SOL $100 1/28 P = ~$15.5m (Notional)

Thetanuts ETH Chain - Luna/WBTC/Talgo/WETH Puts = ~ $11m (Notional)

Thetanuts ETH Chain - WBTC/Talgo/WETH Calls = ~ $26m (Notional)

$36,311

DVOL: Deribit’s volatility index

(1 month, hourly)

SKEWS

(Jan. 23rd, 2022 - Short-term and Medium-term BTC Skews - Deribit)

Crypto assets, along with US equities had a turbulent end of week.

Bitcoin spot prices are down 17% since last week.

This has caused implied volatility to rise while skew repriced significantly lower (led by short-term expirations).

Weekly option skew is now -10pts, after briefly approaching -20pts.

30-day option skew is about -8pts and even long-dated 180-day option skew are negative.

Big bearish sell-offs can often overshoot and invite short-term bounces… Very negative weekly option skew could provide “snap back rally” volatility plays.

Something to keep an eye for.

(Jan. 23rd, 2022 - Long-Dated BTC Skews - Deribit)

TERM STRUCTURE

(Jan. 23rd, 2022 - BTC’s Term Structure - Deribit)

Notice the term structure week-over-week has lifted-off higher in the front-end.

The time series chart below shows a flat/backward term structure sustaining its shape.

The recent past has seen term structure flattening to be quickly faded back lower; today we’re in day 3 of a flat term structure… sustainability we haven’t seen in a while.

ATM/SKEW

(Jan. 23rd, 2022 - BTC ATM & Skews for options 10-60 days out - Deribit)

ATM IV (left) is right back near monthly highs. IV has retraced all mid-month selling.

SKEW (right) has had a devastating drop lower, but was likely overshot. As mentioned before, big dips like this can be met with aggressive buying as many traders have been sidelined during BTC rally.

Aggressive dip buyers can quickly turn volatility skew trades profitable.

Open Interest - @fb_gravitysucks

BTC

This weekly expiration was the perfect representation of market sentiment and subdued volume continuation: with only 13k contracts (one of the lowest values seen in months) and a big sell-off in the morning of expiration. Bears got their premium. Calls sold and puts bought has been the winning strategy.

Around 77% of contracts expired worthless.

(Jan 21th , 2022 – BTC Open interest – Deribit)

(Jan 21th , 2022 – BTC Dollar premium – Deribit)

TOP TRADES

With price stuck around $42k for most of the week and the sell-off move only on Friday/Saturday, trades had two way interest.

The first part of the week had “theta collecting strategies”: a disillusioned trader put on a calendar betting on price range between $39k-$43k. Almost $50k theta per day at inception.

With prices losing some grip, a trader placed a strangle to be exposed to both Vega and Gamma without any bias about direction. Perfect timing.

On Friday morning with prices under the psychological level of $40k, a skillful trader took profit on $45k strike puts and then rolled down positions with a positive net premium.

After the first leg down to $38k, a bullish participant bought a bull call spread 300x for June expiration. This is the equivalent to “buy the dip” in options space.

For more insights, follow veteran crypto options trader Fabio on twitter @fb_gravitysucks

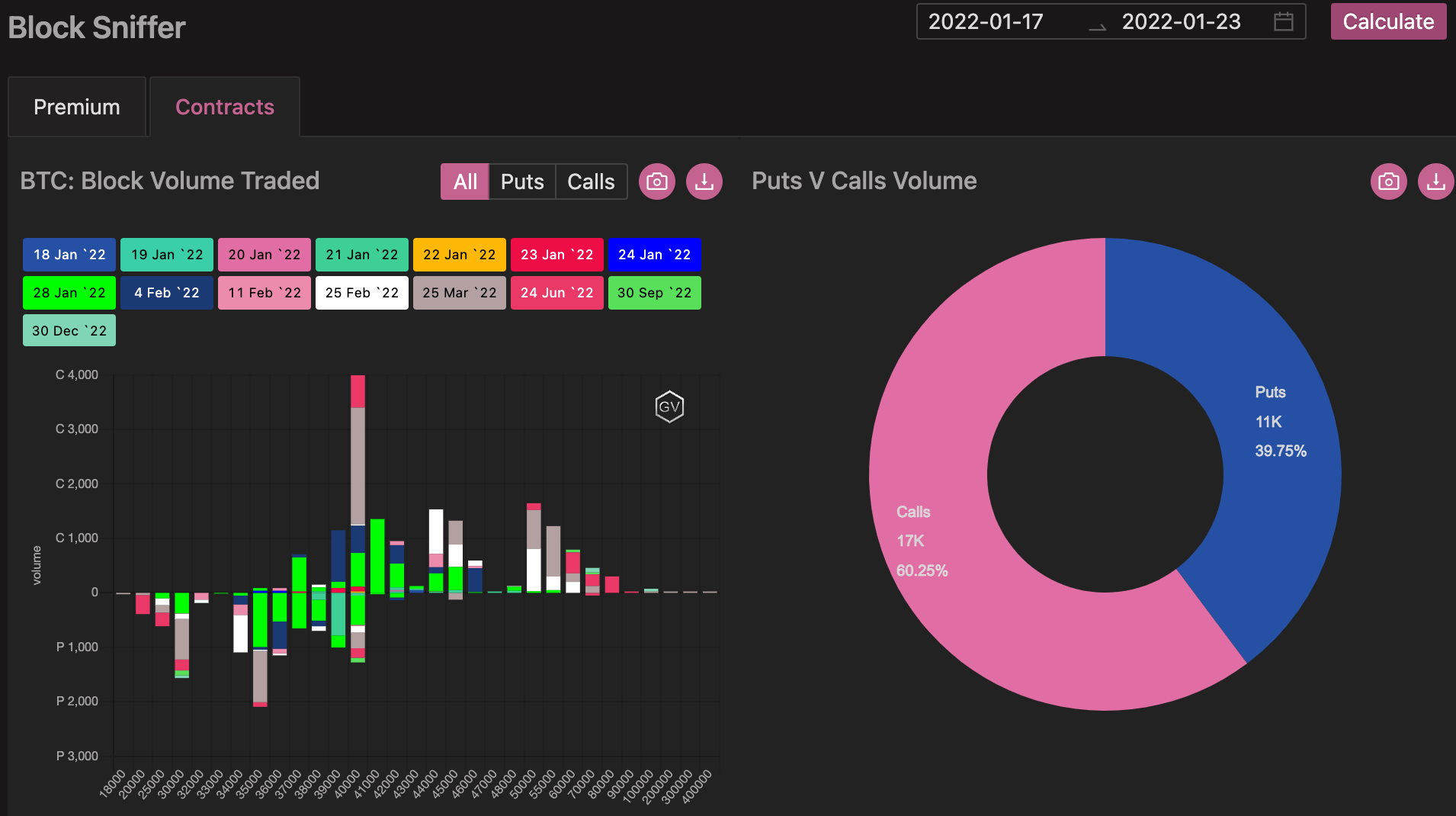

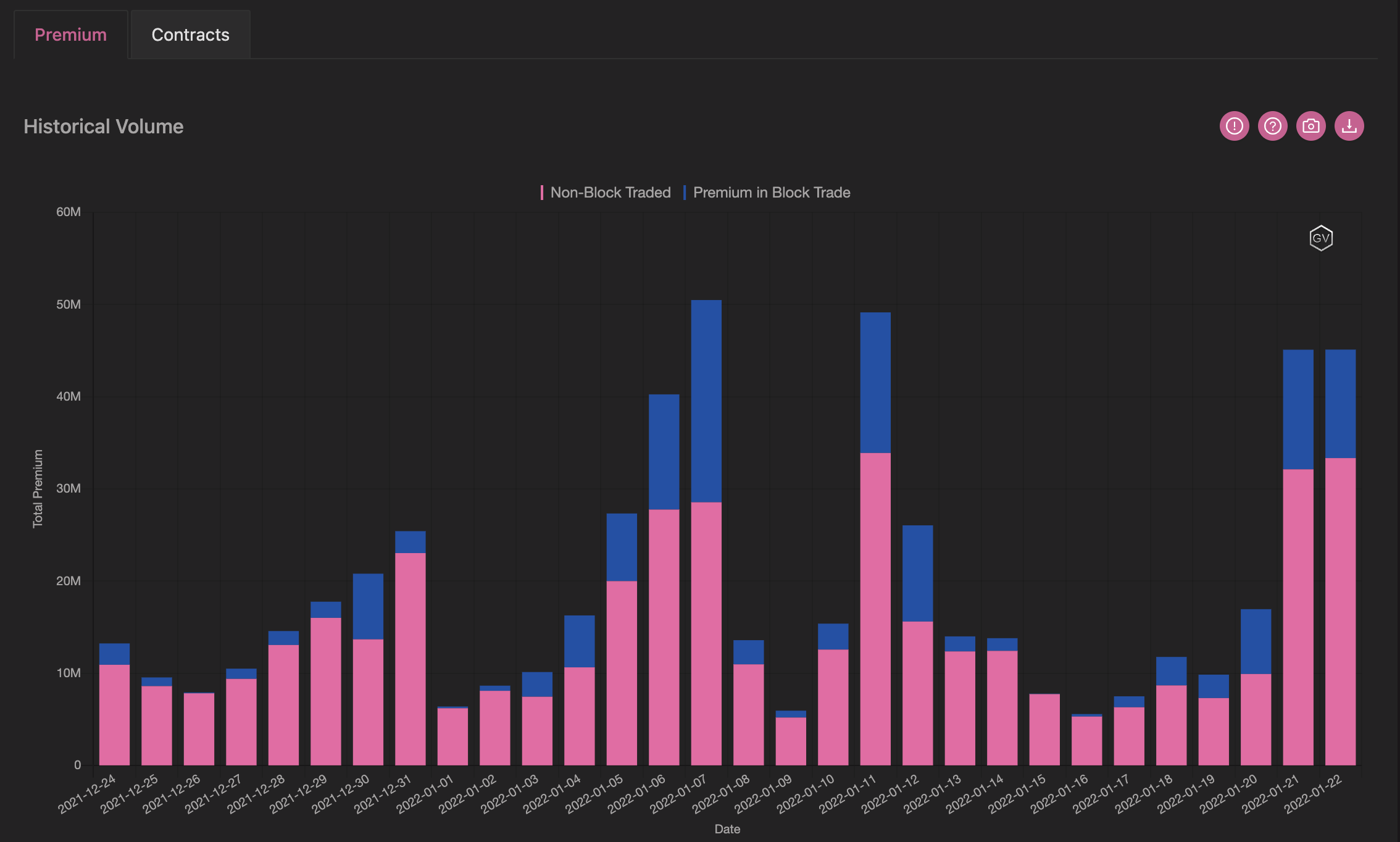

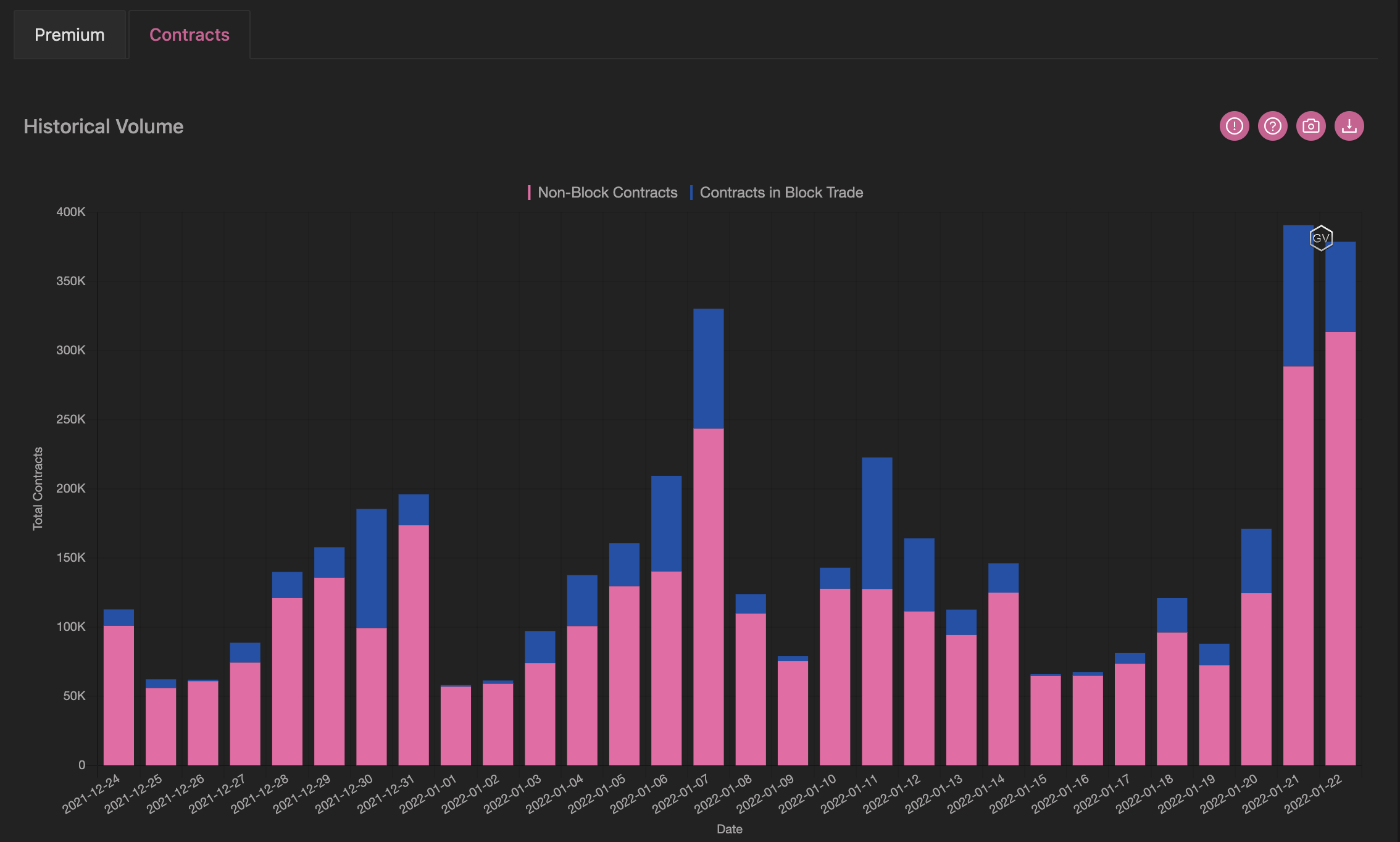

VOLUME

(Jan. 23rd, 2022 - BTC Premium Traded - Deribit)

(Jan. 23rd, 2022 - BTC’s Contracts Traded - Deribit)

Paradigm Block Insights (Jan 17 to Jan 23) - Patrick Chu

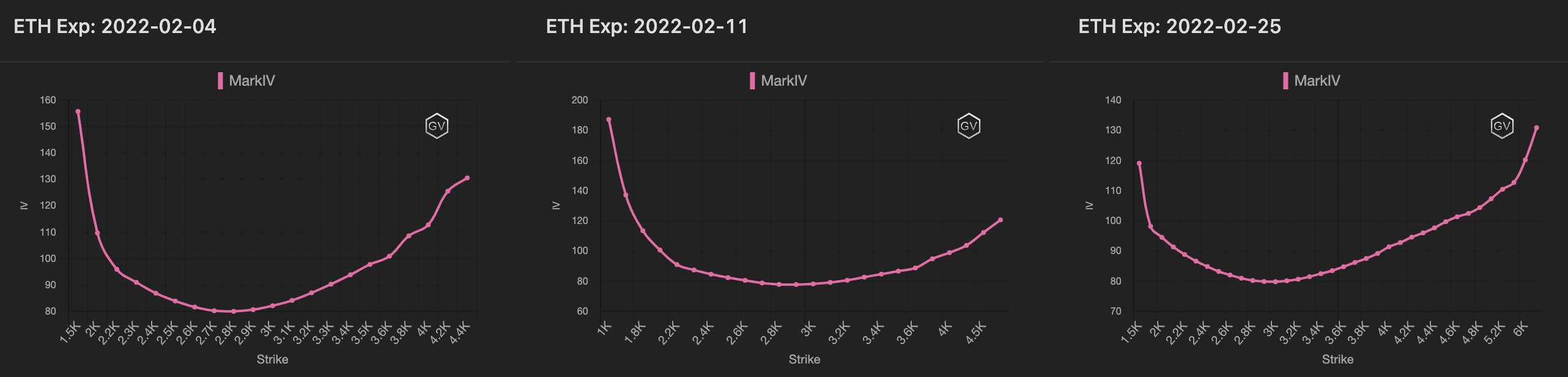

As market sentiment turned sour, BTC & ETH broke the key 39,000 / 2,900 support levels - the short end of the term structure which had been suppressed by DOV selling spiked higher as the curve flattened in both BTC & ETH.

In both BTC & ETH IV moved aggressively higher with 1W vol jumping from 53 to 82 in BTC & 60 to 102 in ETH. Skew also moved in favor of puts, with 25D’s dropping as low as -17 in ETH and -12 in BTC before normalizing into the weekend.

(Jan 17 to Jan 23 - Volume Profile - Deribit & Paradigm)

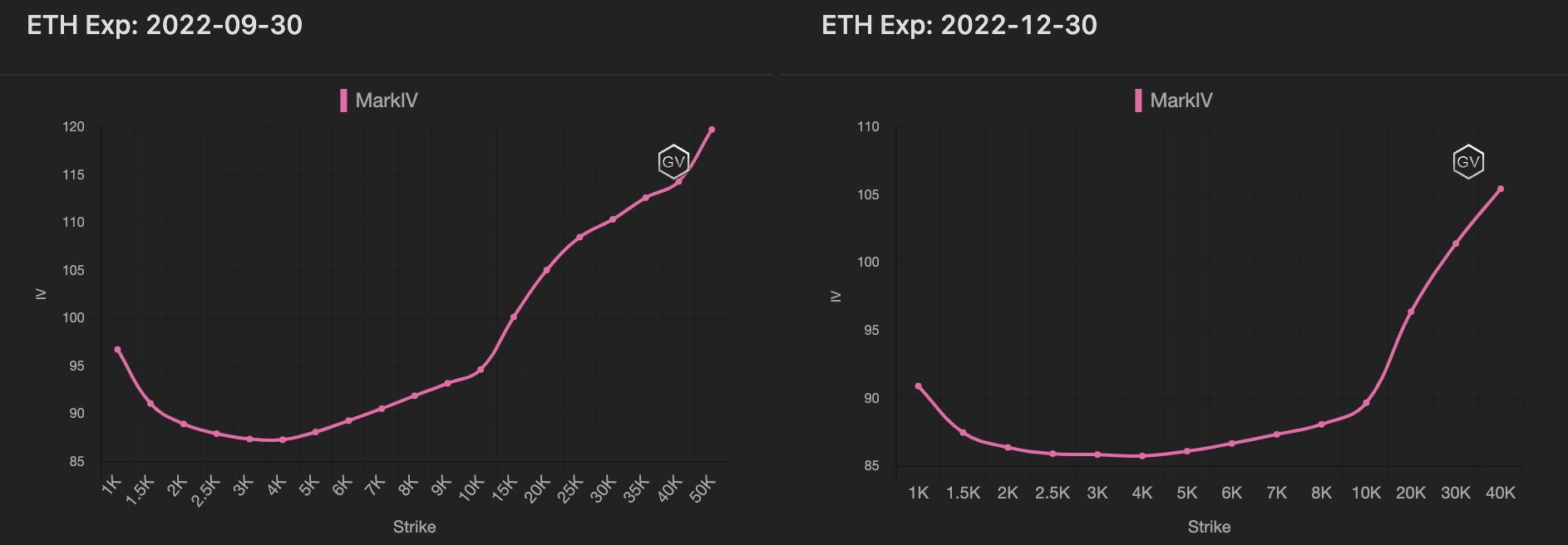

Interestingly, the back end of the curve remained calm given the movements in spot with IV for tenors beyond 1M jumping only 5-7 handles in BTC & ETH, highlighting the structural offer that remains with market supply in overhang.

In BTC this week, the largest volumes came from two-way interest on strangles/straddles, call spreads & outrights. 28Jan 36k/40k and 4Feb 36k/40k were the most popular strangles, while call calendars rolling positions from Jan/Feb to Mar especially on the 40k strike dominated volumes.

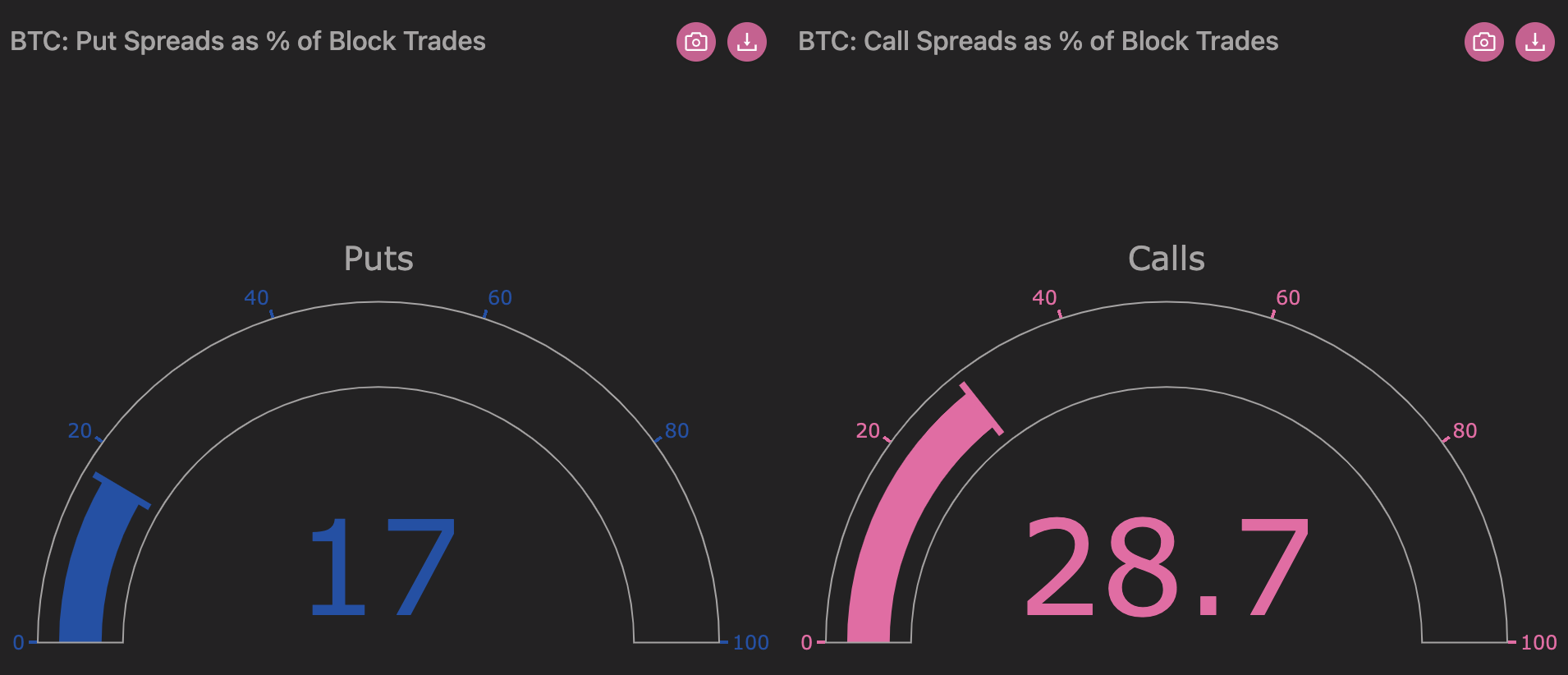

For outright puts on the 21Jan, 28Jan & 25Mar, expiries with strikes between 30k and 38k were popular; puts accounted for almost 40% of total trading volumes.

(Jan 17 to Jan 23 - Put & Call vertical as % of trade “count” - Deribit & Paradigm)

Feel free to contact us at https://t.me/tradeparadigm & follow us at @tradeparadigm on Twitter to access the best pricing and liquidity for large trades in crypto derivatives.

VOLATILITY CONE

(Jan. 23rd, 2022 - BTC’s Volatility Cone)

RV saw significant liftoff, but the volatility cone keeps things in perspective.

Current RV measurements aren’t even over the 75th percentile.

BTC can easily move even more erratically, a good context for vol. traders.

REALIZED & IMPLIED

(Jan. 23rd, 2022 - BTC’s 10-day Realized-, and Trade-Weighted-, Implied-Vol.-Deribit)

RV liftoff was met with similar liftoff in the IV space.

Although the IV move felt large, we’re merely back to the summer 2021 ATM IV VWAP range.

$2,537

DVOL: Deribit’s volatility index

(1 month, hourly)

SKEWS

(Jan. 23rd, 2022 - ETH’s Skews - Deribit)

ETH option skew has seen an even more erratic weekly expiration, reaching nearly -30pts.

30-day options are about -10pts while longer term (180-day) skews are hovering near at par.

(Jan. 23rd, 2022 - ETH’s Skews - Deribit)

TERM STRUCTURE

(Jan. 23rd, 2022 - ETH’s Term Structure - Deribit)

The ETH term structure is significantly higher week-over-week.

The move higher was led by the short-end but the longer-term stuff also saw a parallel shift higher.

Like with BTC, we’re seeing a sustained flat/backward term structure.

Interesting to note: the slight pullback in IV on Jan 21 near the DOV auction schedule… although it’s hard to jump to any conclusions, given the nature of erratic moves like this.

ATM/SKEW

(Jan. 23rd, 2022 - ETH’s ATM & Skews for options 10-60 days out - Deribit)

ATM IV (left) is right back to monthly highs (yet not exceeding them).

Skew (right) is showing a holding pattern near the lows for these select expirations.

Open Interest - @fb_gravitysucks

ETH

This weekly expiration was in line with recent averages with around 136k contracts, 78% of whom expired worthless. The same considerations seen for Bitcoin apply here: volumes subdued, two-way interest for puts and calls sold. Bears in control got paid.

(Jan 21th , 2022 – ETH Open interest– Deribit)

(Jan 21th , 2022 – ETH Dollar premium – Deribit)

TOP TRADES

Participants have lost some interest in ETH trades. Talking for months about the flippening of the market cap and the flippening of options volumes has been a curse at this point.

Nevertheless, some interesting trades hit the tape.

With prices above the $3k support level, an experienced trader bought the bounce with a sort of risk-reversal, selling 3k puts and buying 7k calls, with protection for gamma/vega exposure risk in 1.5k strike.

After the break down of 3k support level, a participant bought 6500 bull call spreads for June. As is often the case with prices near the marks, the direction of trade labels have been reversed.

For more insights, follow veteran crypto options trader Fabio on twitter @fb_gravitysucks

VOLUME

(Jan. 23rd, 2022 - ETH’s Premium Traded - Deribit)

(Jan. 23rd, 2022 - ETH’s Contracts Traded - Deribit)

ETH option volumes are holding relatively steady.

Paradigm Block Insights (Jan 17 to Jan 23) - Patrick Chu

In ETH this week, the market dropped; we saw strong interest for topside call spreads, most notably 24 Jun 1x2 10000C/20000C, which traded 10500x by 21000x, dominating volumes.

We also saw significant interest for 24 Jun 3000/5000 call spreads towards the end of the week.

Other notable interests this week that traded significant volumes included the 28Jan 3000P/2700P put spread, as well as the 25Mar 2000C/5000P risk reversals, as market sentiment remained resilient in face of weakness.

(Jan 17 to Jan 23 - Volume Profile - Deribit & Paradigm)

(Jan 17 to Jan 23 - Put & Call vertical as % of trade “count” - Deribit & Paradigm)

Feel free to contact us at https://t.me/tradeparadigm & follow us at @tradeparadigm on Twitter to access the best pricing and liquidity for large trades in crypto derivatives.

VOLATILITY CONE

(Jan. 23rd, 2022 - ETH’s Volatility Cone)

ETH RV actually exceeds the 75th percentile for the weekly measurement window.

REALIZED & IMPLIED

(Jan. 23rd, 2022 - ETH’s 10-day Realized -, and Trade-Weighted-, ImpliedVol.-Deribit)

ETH RV is exceeding IV, even despite IV coming in higher week-over-week.

As we noted last week, the ETH / BTC IV gap has shrunk significantly… Combine the relative vol with the RV/IV discount… Long ETH volatility could still be interesting given the right structure.