Crypto Options Analytics, August 29th, 2021

Rich implied vol. complex, look for short volatility structures

Visit gvol.io

Disclaimer: Nothing here is trading advice or solicitation. This is for educational purposes only.

Math minded people here, pardon any typos.

| Twitter")

Feel free to contact us at https://t.me/tradeparadigm & follow us at @tradeparadigm on Twitter to access the best pricing and liquidity for large trades in crypto derivatives.

$48,827

DVOL: Deribit’s volatility index

(1 month, hourly)

SKEWS

(Aug. 29th, 2021 - Short-term and Medium-Term BTC Skews - Deribit)

Volatility is continuing to leak out of the market.

Option skews fell drastically from last week. Short-term and medium-term options are trading at symmetry (~0 skew).

BTC spot prices saw resistance this week around the $50k price level. This resistance has caused option traders to sell the call skew down as the likelihood for a continued fast rally higher has diminished.

Long-term option skews remain strong. Call preference continues to be displayed through higher call implieds.

(Aug. 29th, 2021 - Long-Dated BTC Skews - Deribit)

TERM STRUCTURE

(Aug. 29th, 2021 - BTC’s Term Structure - Deribit)

The term structure continues to display a steep Contango structure.

Although the short-end of the curve is the cheapest, even these maturities are trading at a large premium to realized volatility.

Overall, the implied vol. complex is priced richly. There are short vol. trades to be done across the curve.

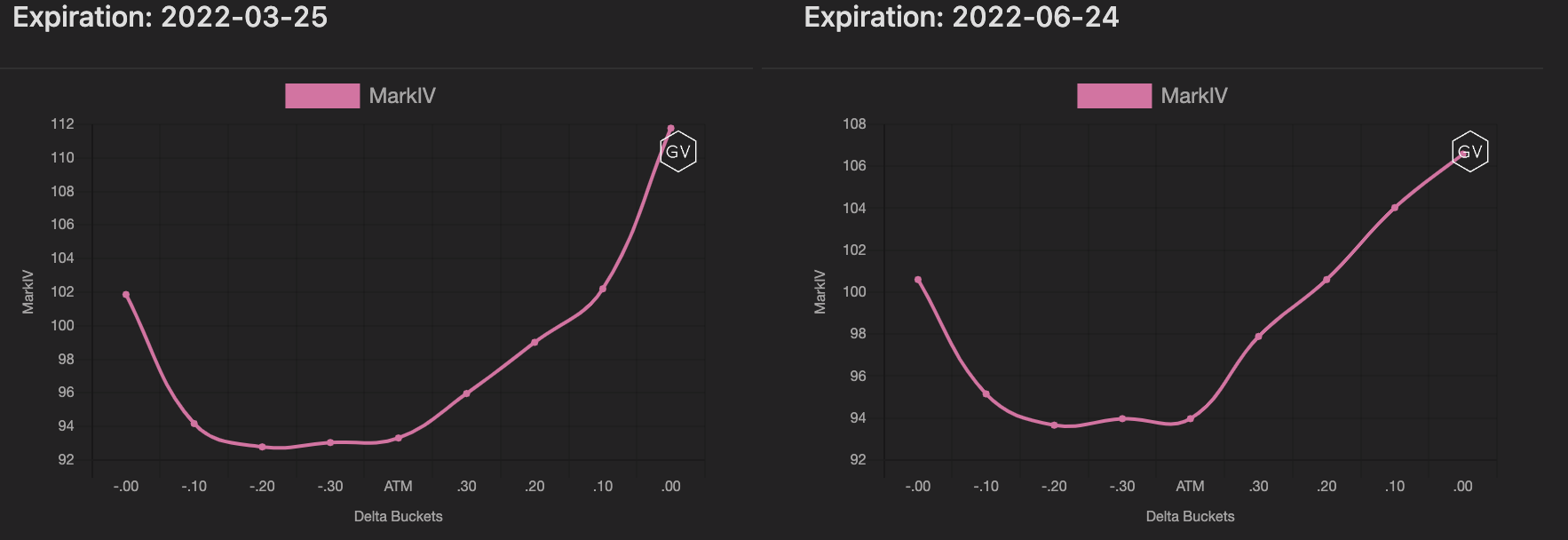

ATM/SKEW

(Aug. 29th, 2021 - BTC ATM & Skews for options 10-60 days out - Deribit)

ATM IV (left) hasn’t moved, although this tranquil activity continues to provide Theta decay and Vega roll down

Skew (right) has dropped significantly. IV skew is no longer pricing the potential for an explosive upside rally in the short-term.

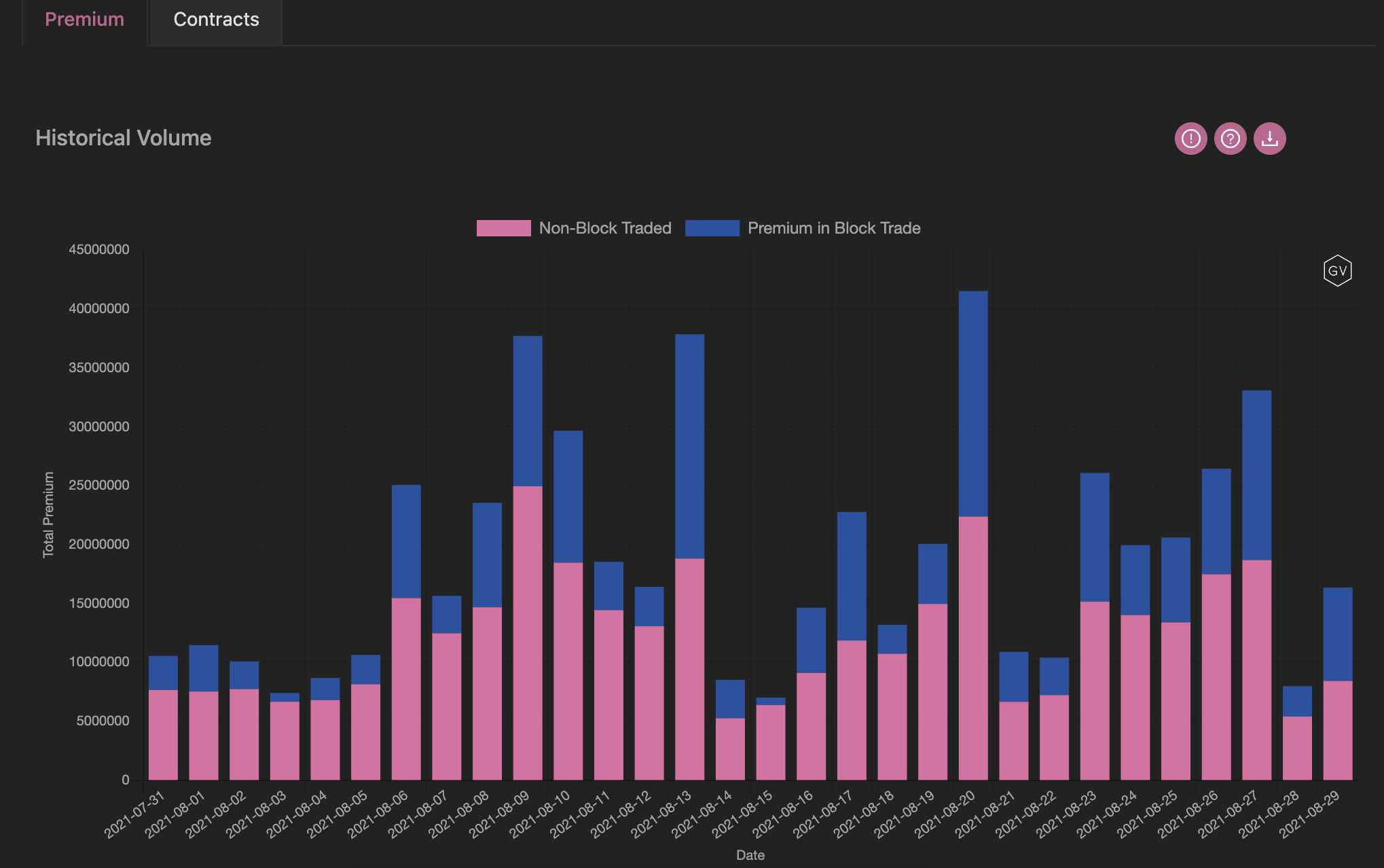

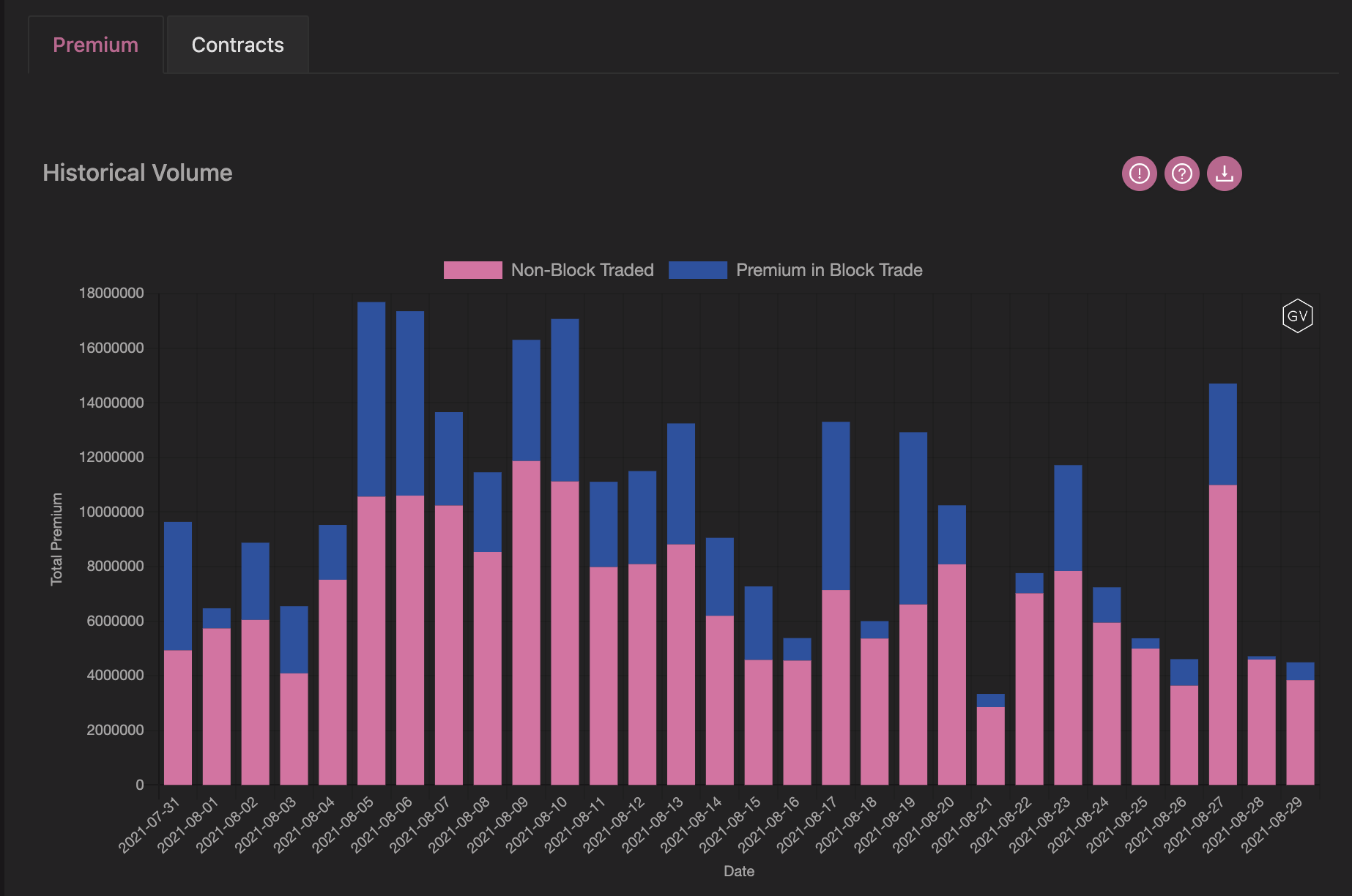

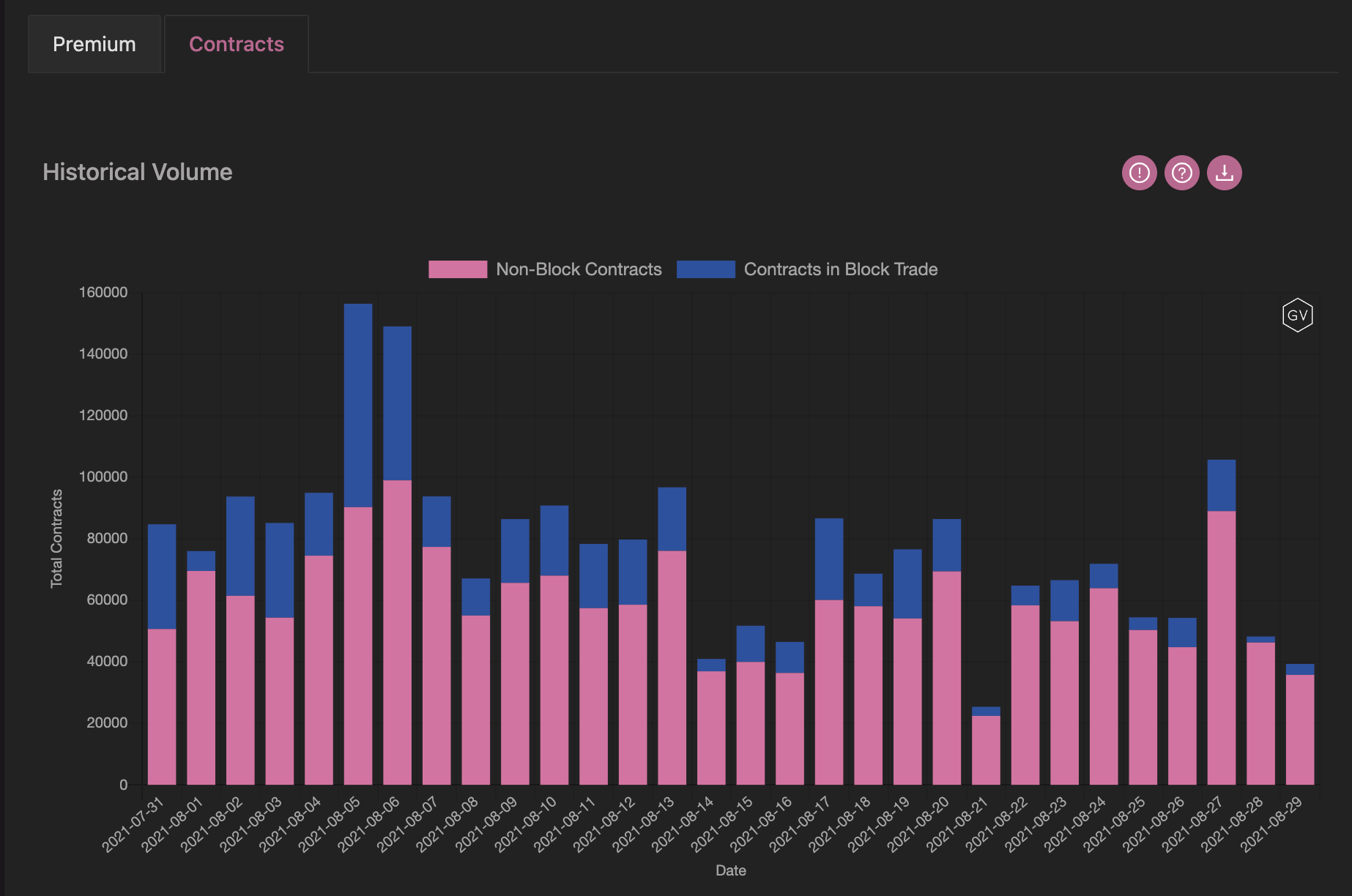

VOLUME

(Aug. 29th, 2021 - BTC Premium Traded - Deribit)

(Aug. 29th, 2021 - BTC’s Contracts Traded - Deribit)

Overall, volumes were similar to last week.

Most of the differential can be found in the volatility surface this week, with little insight to be gained from volume activity levels.

VOLATILITY CONE

(Aug. 29th, 2021 - BTC’s Volatility Cone)

Realized volatility remains low.

The lower 25th percentile currently represents most of the realized volatility readings but RV can very much drop even lower.

REALIZED & IMPLIED

(Aug 29th, 2021 - BTC’s 10-day Realized-, and Trade-Weighted-, Implied-Vol.-Deribit)

The LARGE IV to RV premium continues once again this week.

Not only does the premium continue to hold, but it looks to have gotten even wider this week.

$3,230

DVOL: Deribit’s volatility index

(1 month, hourly)

SKEWS

(Aug. 29th, 2021 - ETH’s Skews - Deribit)

Ethereum has witnessed a drop in short-term and medium-term option skews.

The current option skew readings are now ~0% for these select maturities.

The enthusiasm for upside optionality has diminished this week, although long-term options continue to display increased demand for call options.

(Aug. 29th, 2021 - ETH’s Skews - Deribit)

TERM STRUCTURE

(Aug. 29th, 2021 - ETH’s Term Structure - Deribit)

The term-structure remains VERY steep.

The Contango shape has a pronounced “kink” at the December 2021 expiration, which provides an abnormally expensive/rich implied volatility.

Nearly every point along the term structure provides interesting short vol. opportunities, given the current RV environment.

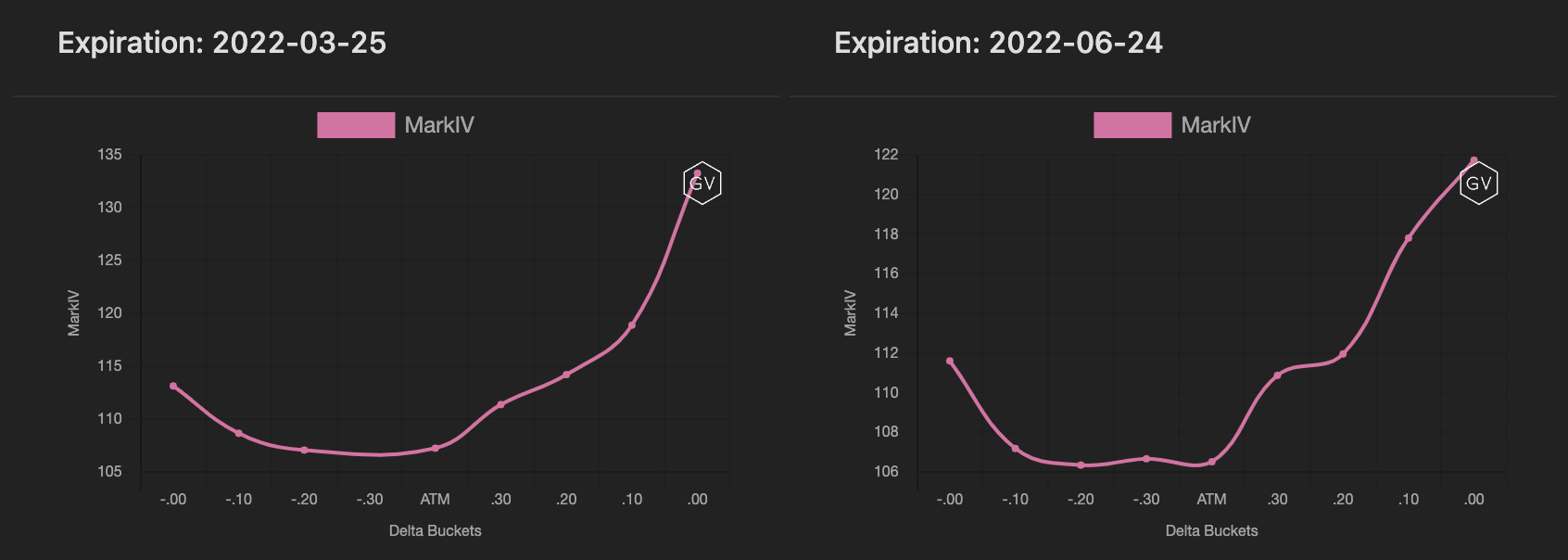

ATM/SKEW

(Aug. 29th, 2021 - ETH’s ATM & Skews for options 10-60 days out - Deribit)

ATM IV (left) continues a steady drop lower, despite BTC seeing ATM IV consolidate this week.

SKEW (right) has dropped a lot over the past week. Like BTC, ETH option skew currently hovers around the ~0 line for selected maturities.

VOLUME

(Aug. 29th, 2021 - ETH’s Premium Traded - Deribit)

(Aug. 29th, 2021 - ETH’s Contracts Traded - Deribit)

ETH volumes have diminished a lot over the past week.

This volume activity provides good context to the diminishing IV theme witnessed this past week.

VOLATILITY CONE

(Aug. 29th, 2021 - ETH’s Volatility Cone)

ETH RV continued lower.

Many of the RV measurement windows are now trading BELOW the lower 25th percentile.

REALIZED & IMPLIED

(Aug. 29th, 2021 - ETH’s 10-day Realized -, and Trade-Weighted-, ImpliedVol.-Deribit)

Implied Vols. have held relatively strong compared to the diminishing RV activity.

These two developments have caused the IV/RV premium to become rather wide, allowing room for IV to drop lower if RV doesn’t change course going forward.

great stuff ... what do you use the volatility cone for? Is there a sentiment read to be had there?